November 2025

Broward County Market Update

Broward County’s November 2025 numbers reflect how today’s market is balancing buyer choice with steady demand. Year-over-year comparisons highlight where pricing is holding firm, where inventory is building, and how quickly homes are moving—helpful context whether you’re planning to buy, sell, or simply track local trends.

Broward County Single-Family Homes

-

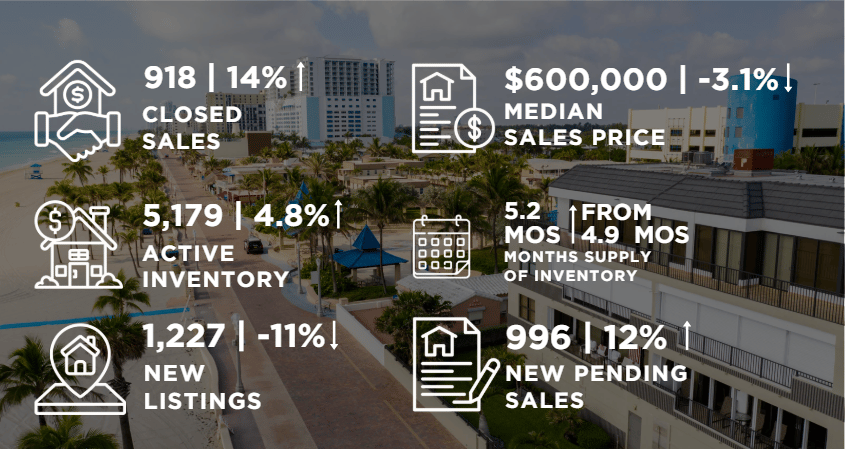

Closed Sales: 918 (+14% YoY) — More sales closed compared to last November, signaling resilient buyer activity.

-

Median Sales Price: $600,000 (-3.1% YoY) — Prices eased slightly year-over-year, suggesting buyers are gaining a bit more leverage on pricing.

-

Active Inventory: 5,179 (+4.8% YoY) — Inventory rose, expanding options for buyers and increasing competition among listings.

-

Months’ Supply of Inventory: 5.2 months (up from 4.9 a year ago) — Conditions are leaning closer to a more balanced market than last year.

-

New Listings: 1,227 (-11% YoY) — Fewer new homes came to market, which can limit fresh selection despite higher overall inventory.

-

New Pending Sales: 996 (+12% YoY) — Pending activity improved, indicating ongoing demand and a solid pipeline of future closings.

Single-family home demand strengthened, while a modest rise in inventory and months’ supply is helping cool price pressure. Sellers can still do well—especially with strong presentation and accurate pricing—while buyers may find more negotiating room than a year ago.

Broward County Townhouses and Condos

-

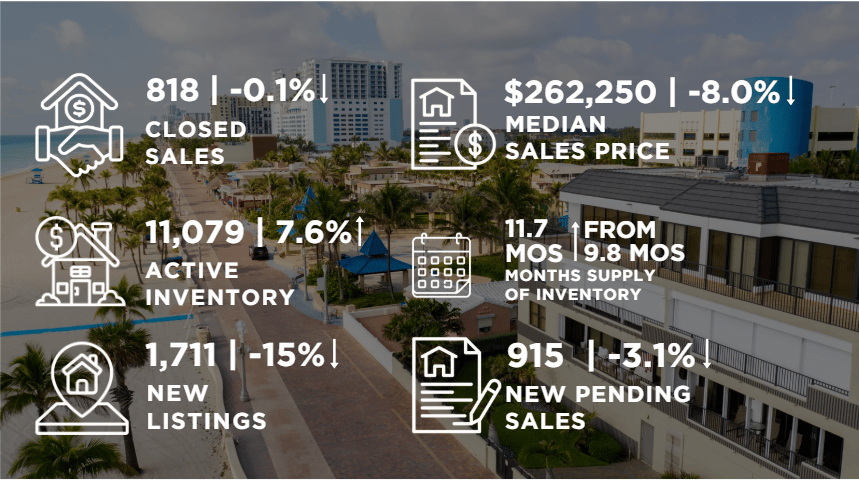

Closed Sales: 818 (-0.1% YoY) — Essentially flat, showing steady transaction volume year-over-year.

-

Median Sales Price: $262,250 (-8.0% YoY) — Prices pulled back more noticeably, pointing to increased buyer sensitivity and competition among listings.

-

Active Inventory: 11,079 (+7.6% YoY) — More available units are giving buyers more choice across communities and price points.

-

Months’ Supply of Inventory: 11.7 months (up from 9.8 a year ago) — A higher supply level suggests a slower-moving segment with more negotiating power for buyers.

-

New Listings: 1,711 (-15% YoY) — New listing flow slowed, but overall inventory remains elevated.

-

New Pending Sales: 915 (-3.1% YoY) — Pending activity dipped slightly, consistent with a market that’s taking longer to convert interest into contracts.

The townhouse and condo segment is providing buyers with substantial options, and pricing has adjusted accordingly. Sellers may need sharper pricing strategies and standout condition to capture attention, while buyers can be more selective and negotiate more confidently.